Economic Recovery And Growth Plan, 2017-2020: From Recession To Recession

Since gaining independence in 1960, Nigeria has initiated series of development plans aimed at directing the utilisation of the country resources into different development programmes and activities in accordance with National priorities, one of these is the Economic Recovery and Growth Plan (ERGP) launched in 2017. ERGP is a Medium-Term Plan for 2017 and 2020, with three broad strategic objectives of restoring growth by ensuring macroeconomic stability and economic diversification; investment in people through the creation of opportunities and support to the vulnerable by increasing social inclusion, creating jobs, and improving the human capital base of the economy; and building a globally competitive economy by investing in infrastructure, improving the business environment, and promoting Digital-led growth.

Recall that in January 2016, the Oil price drop to $26 per barrel. This was against the oil revenue projection predicated on a benchmark oil price of $38pb in that fiscal year (MTEF, 2014-2016). As of the second quarter of 2016,Nigeria slipped into recession with a GDP of -2.06% after two consecutive negative growth due to the impact of low oil prices which significantly reduced government revenues, weakened the naira, and increased inflationary pressure. In the year, the exchange rate rose from N197/$ in January to N348/$ in August. Inflation also rose from 11.35% in February to 18.3% in October and 18.48% in November. Thus, at the end of the year, unemployment had risen to 14.2%, life expectancy at birth was at 53.4 years and the poverty level was 38.1% (World Bank 2016). While thecountry experienced a balance of trade deficit that year, the Real GDP growth stood at -1.6. Correcting this socioeconomic situation and move Nigeria into the path of growth were the basis for the emergence of the ERGP in 2017.

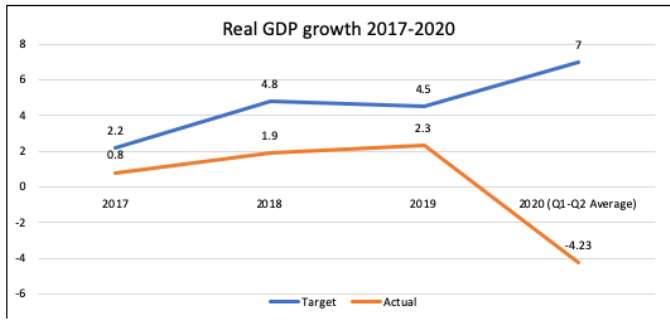

With focused on the six sectoral priorities namely agriculture, manufacturing, solid minerals, services, construction and real estate, and Oil and gas, the Economic and Recovery Growth Plan (ERGP) projected the Real GDP growth to improve significantly to 2.19 per cent in 2017, reaching 7 per cent at the end of the Plan period in 2020. It could be seen from the below that the Real GDP only grew to 0.8 in 2017, the average Real GDP growth in Q1 (1.87%) and Q2 (-6.10%) of the 2020 fiscal year stood at -4.23%.

Also, the inflation rate which was projected to trend downwards from almost 19 per cent to single digits by 2020 has not been achieved. The current inflation rate as of the third quarter of 2020 is double-digit.

More so, it was projected that the exchange rate would stabilise as the monetary, fiscal, and trade policies are fully aligned, the exchange now stood at N467/$ in Nigeria Black Market today and the official rate stands at N379/$.

The electricity which was predicted at driving growth and expansion in all other sectors has not improved as millions of households still live without electricity and most multinational and local industries depend mostly on the generator. Despite this challenge, there was a hike in the electricity tariff, a move considered by Nigerians as untimely and wicked.

The ERGP sought to create an industrialised economy through a strong recovery and growth in the manufacturing; SMEs, services sectors, agro-processing, and food and beverage manufacturing. However, in the overall, the NERGP estimates an average annual growth of 8.5 per cent in manufacturing, to rise from -5.8 per cent in 2016 to 10.6 per cent by 2020. Today, the Real growth rate in the manufacturing sector is only 0.43 in Q1 and –8.78% in Q2, on average, the growth rate is -4.175% in both quarters against the 10.6% target.

It is also expected that over 15 million jobs would be created during the Plan horizon or an average of 3.7 million jobs per annum with particular reference to youth employment and ensuring that youth are the priority beneficiaries. In a report published by the Nigeria Economic Summit Group (NESG) in 2019, it was noted that between 2015 and 2018, an average of 4.8 million individuals entered into the labour market while only 625,000 net jobs were created (NESG, 2020). In December the same year, the World Bank reported that five million (5 million) Nigerians joined the labour force in 2018 while only 450,000 of them were employed. From the two-report, it can be concluded that the projected 3.7 million average projected in the ERGP has not been achieved. Despite the efforts, the unemployment among the youth age 15-34 increased from 19.4% in Q$ 2016 to 29.7% in Q3 2018.

The increase in the unemployment rate could be attributed to many factors including the disparity between the population growth and the economic policy. It is believed that the population is growing at a rate of 3% (NBS, 2017) without a corresponding job opportunity. This has also made the government projection of reducing unemployment rate from 13.9 per cent as of Q3 2016 to 11.23 per cent by 2020 unrealistic as the unemployment rate increased from 13.9% in Q3 2016 to 27.1% Q2 2020.

Like many of its preceding development policies, the NERGP development plan has failed to transform the nation and set it on the path of development. While it was able to move the country out of recession in 2017, the recent collapsein oil prices coupled with the COVID-19 pandemic may slip the country into another recession if the real GDP growth enters into another negative growth in the third quarter of 2020. This may therefore worsen the situation given the poor culture of economic diversification, plan indiscipline and unnecessary partisanship, inadequate feasibility studies in planning, lack of comprehensive statistics data, geometric growth in population defeating the essence of economic forecasting in plan formulation and implementation, high cost of governance, etc.

However, with the current Economic Sustainability Plan (ESP) recently launched, no meaningful changes may be expected if we do not dissect from the culture of fiscal indiscipline, monolithic economy, contract inflation, poor resources mobilisation for its realization.

While ensuring public-private partnership for growth and development, the government must also ensure sanity in the public sector toward ensuring adequate and timely resource mobilisation without prejudice. Prioritization of the critical non-oil sector of the economy namely agriculture, manufacturing, solid minerals, services, etc. need to be given more attention at all levels.

Lastly, it is high time to come up with regulation that mandates government officials at all levels to use local contents. This will encourage others to follow suite, thereby reduce pressure on the dollar and grow our local industries for viable development.

Kareem Abdulrasaq writes from Ilorin, Kwara State [email protected]